The ECB anticipates average inflation of 6.3% in 2023 and 3.4% in 2024, with rates expected to approach 2% by the end of 2024. Consequently, the normalization of ECB rates should begin around that time.

Recent events in the banking market (SVB, Credit Suisse, First Republic…) do not call into question the current monetary policy.

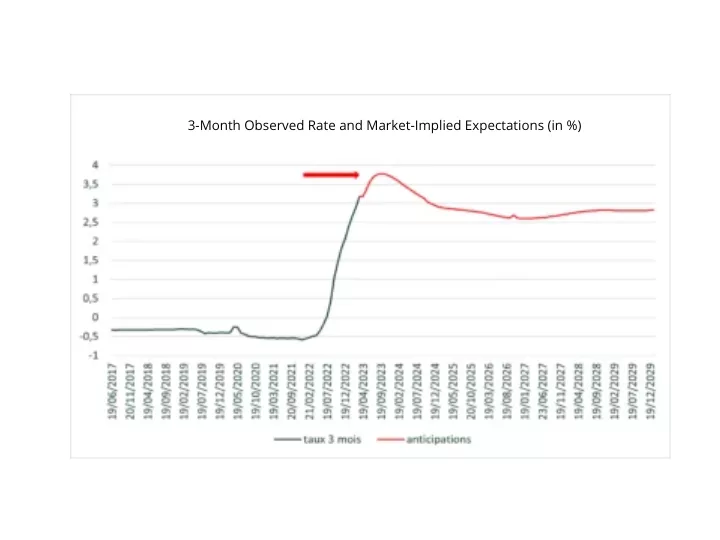

On Thursday, May 4th, the European Central Bank (ECB) announced, for the seventh consecutive meeting, a rate hike of 0.25 percentage points, bringing the deposit rate to 3.25%. While this does not yet signal the end of monetary tightening in the eurozone, it does represent a slowdown.

As such, according to specialists’ expectations (see chart), rates are not expected to remain indefinitely high.

Which investments should be chosen to lock in high-rate levels while maintaining short-term availability of funds?

One solution to secure high interest rates is to opt for fixed-rate term deposits over longer maturities.

These products offer simplicity of implementation, allowing investors to lock in their capital for a defined period. However, this approach is limited to the maturity of the deposit, meaning that investors will not be able to benefit from any potential further rise in interest rates should it persist beyond the agreed term.

A more suitable solution is to set up capitalisation contracts with an investment in an insurer’s euro-denominated fund.

The mechanism of this type of contract works as follows: the insurer invests in long-maturity bonds and guarantees the investor 100% capital protection at all times, with fund availability within 15 days. The returns offered by these contracts are generally above 4.00% and are expected to increase in the coming years, as insurers incorporate fixed-rate, long-maturity, high-yield bonds into their portfolios.

Investing in the euro-denominated fund of a capitalisation contract offers several advantages.

First of all, locking in high yields over the long term, providing investors with a degree of stability. Unlike term deposits, this solution offers the ability to benefit from potential future interest rate increases. By investing through an insurer, investors also diversify their risk compared to traditional bank deposits.

Lastly, the liquidity offered by capitalisation contracts is generally greater than that of term deposits, with funds available within 15 days.

To set up an investment in a capitalisation contract, it is recommended to turn to a qualified professional. These experts will be able to assist investors in selecting contracts suited to their needs. The Fintis team is at your disposal to support you in setting up capitalisation contracts.